Entravision (EVC) ENG

Entravision is an American media and marketing company. The investment thesis for this company has three pillars:

a legacy segment of Spanish-language television stations and radio stations focused on the Hispanic population in the US

assets in the form of radio spectrum that could be sold

a rapidly growing segment of advertising in the digital space, represented by their companies Smadex and Adwake,

Media segment

Entravision operates dozens of television and radio stations that focus on Hispanics in the US. In the era of VOD platforms and other forms of media digitization, the market perceives this business as a declining segment that will gradually disappear in the long term. I agree with this, but even a company that is gradually dying can be a good investment if it is cheap enough and management allocates capital well.

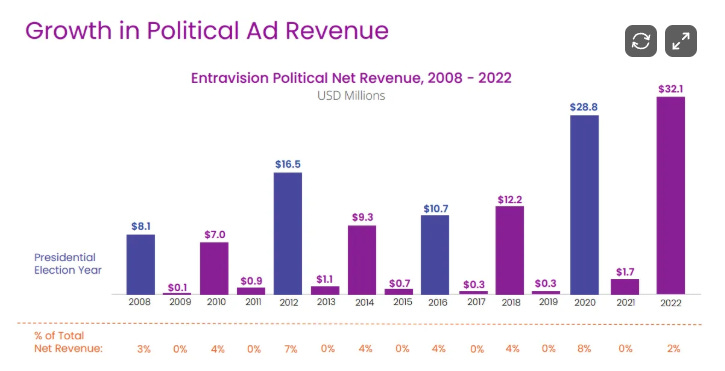

The company currently operates in such a way that in even-numbered years, when there are either presidential or midterm elections, it makes a profit thanks to political advertising, and in odd-numbered years, it is currently at break-even or a slight loss. The midterms in 2026 will have a positive impact on the company’s profitability. At the same time, Entravision is trying to streamline and restructure its media segment, which involves some additional costs that could eventually end. In addition, the company is paying off debt, which also represents some costs. We will talk more about debt later.

It is difficult to imagine how much the media segment will earn once it completes its restructuring and repays its debt, and I honestly have no ambition to try to estimate this. However, it pays a dividend of about 6.8%, which I believe is sustainable. The media segment is not the most important part of my investment thesis, but I think it still represents positive value.

This graph shows revenue from political advertising, and you can see how it increases during election years. At the same time, I expect Entravision to raise its advertising prices, which should at least partially reflect inflation.

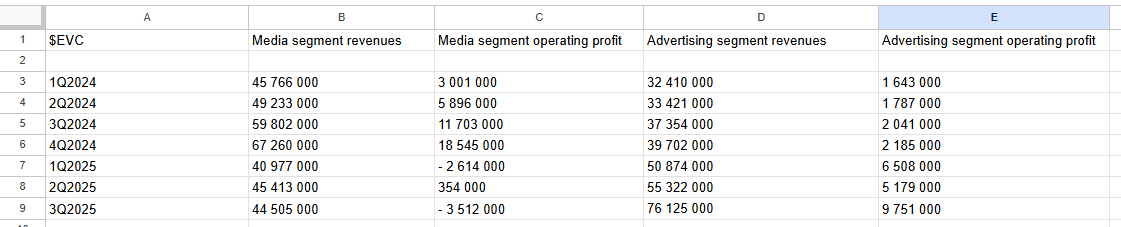

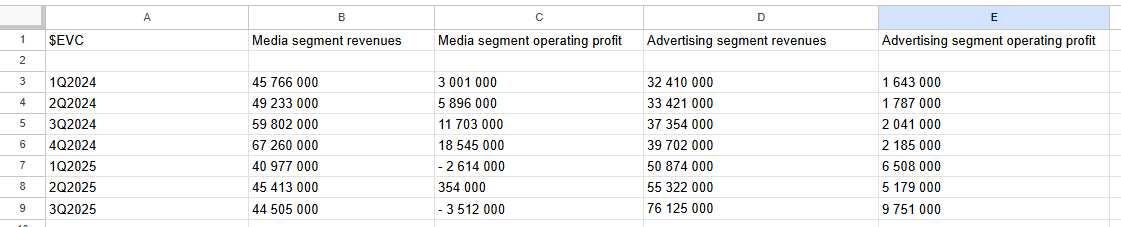

Here is a table showing Entravision’s revenues and profits. The left columns labeled “media segment” are for the legacy media business. We can see that over longer periods of time, this segment is profitable. In the third and fourth quarters of 2024, advertising revenue from the presidential election is reflected, while in the first and third quarters of 2025, the segment was at a loss. It should be noted that there were also some one-off items. The midterm elections in 2026 should then be a tailwind for Entravision’s business.

Broadcast spectrum

Entravision also owns part of the broadcasting spectrum, which is a relatively rare asset. In addition to television and radio broadcasting, the spectrum is also valuable to telecommunications companies and the public sector. It is difficult to say whether there is a real ambition to sell it. I have no opinion on the valuation of the spectrum, so I borrowed the valuation from external analyses, where the spectrum was last auctioned in 2017 and, based on the prices at that time, Entravision’s entire spectrum is worth around $270 million. If we adjust for inflation, it comes to approximately $380 million.

At the same time, the Trump administration, represented by the new chairman of the Federal Communications Commission, Brandon Carr, is more open to potential spectrum sales than the previous administration.

Ad-tech segment

And now for the most important part of the investment thesis on Entravision. Entravision encompasses a rapidly growing segment specializing in online advertising represented by Smadex and Adwake. These companies are engaged in optimizing and targeting advertising in the digital space. Like any other company, you hire these companies to achieve the highest possible reach in your target group for the money you pay for advertising. In simple terms, this means that advertisements for your products are displayed to people who, based on their previous behavior in the virtual space, may be interested in them. You know when you type “refrigerator” into a search engine and then ads for refrigerators pop up everywhere for two weeks? That’s it.

Once again, I will pull out my self-made table. The advertising segment columns are specifically for this ad-tech segment. As you can see, the segment is growing rapidly and operational leverage is kicking in. In the last quarter, they reported extraordinary growth of 104% YoY in revenue and 378% in EBITDA. That is absolutely insane growth. I have no idea if the next quarters will be the same, but I am generally optimistic about future developments.

I took a closer look at ad-tech companies. It seems to me that they have quite a few customers from emerging markets, such as South America or the Middle East, where they might have an edge over their competitors. I was surprised that Smadex and Adwake are headquartered in Spain. If you look at the LinkedIn pages of both companies, you can see that they are hiring new employees quite aggressively. The general trend now is to reduce headcount, so the demand for new employees is a sign to me that business is doing well.

Valuation

Entravision is trading at a market cap of $260 million and with relatively high debt at EV $420 million. I will start with the valuation of the company’s most important segment, its ad-tech segment.

I believe that ad-tech will earn significantly more in the next 12 months than in the past. All we need to do is annualize the last quarter, i.e., 4 x 9,750,000 = $39,000,000 EBITDA. If we apply a multiple of 10x to this figure, we get $390 million, which is almost at the level of Entravision’s EV. I sincerely believe that such a business deserves a much higher multiple, and I can only imagine what the company’s valuation would be if it were not part of a holding company. Add to that the value of the spectrum and legacy business, and we can see that the company is significantly undervalued.

Conclusion

In my opinion, Entravision is an absolutely remarkable investment, which is why it is now the second largest in my portfolio. The company is covered on their X accounts by Oracle of Oslo and Mikro Kap David. I recommend reading their posts on X and Substack.